Retire a Millionaire!

Before I begin...

For this post to be relevant to an international audience, $1,000,000 can be divided by the purchasing power parity (PPP) of each applicable nation.

There are other factors that are involved as well; national economic development, the type of political economy, where a nation is in its debt cycle, etc…

So this post is mostly about the personal habits of being a millionaire, not about the status of the nation-state to foster wealth in its citizens.

Good Habits of Everyday Millionaires:

- Earn more than you spend (savings) - If you spend more than you earn, you have no money left to work for you in an investment.

- Invest early and consistently - Have at least two incomes; you work for an income, and your money works for an income.

- Use credit productively and sparingly - credit encourages people to spend more, faster and less wisely. And debt must be paid back, adding to your expenses, so that money is not in investments, then investments are not working for you.

- Never use credit to invest - Sometimes people use credit to leverage higher returns on investments...then pay the debt off, keeping the profit. This rarely works for the individual investor. Most people are not that smart or lucky to time markets, and most lose considerable amounts of money.

- Have at least a six-month emergency fund - Shit Happens! Your car breaks down, you need a new air conditioner, you have a medical emergency, you lose your job, etc… These things happen to everyone. Having six months worth of expenses in cash prevents you from going into debt when an emergency happens.

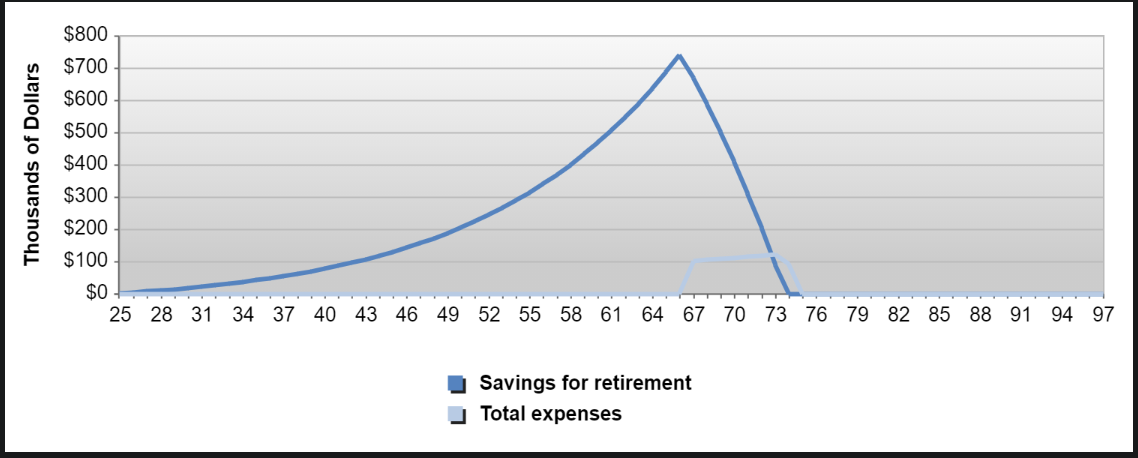

'Sally the Saver' and 'Bob the Spender.'

Sally the Saver:

Beginning at age 24.

Age of retirement is 67.

Annual household income the first year of $50,000

Annual retirement savings is 15% or $625/month (1st year)

Starting year retirement savings is $0

Income increase every year of 2%

2.9% Annual inflation.

7% annual return on investment.

Total retirement of $2,227,052 at age 67.

Annual retirement expenses of $103,376 which is 90% of your last year's income of $114,862.

Retirement savings runs out at age 92.

Not including Social Security benefits.

Bob the Spender

Beginning at age 24.

Age of retirement is 67.

Annual household income the first year of $50,000

Annual retirement savings is 5% or $208/month (1st year)

Starting year retirement savings is $0

Income increase every year of 2%

2.9% Annual inflation.

7% annual return on investment.

Total retirement of $742,351 at age 67.

Annual retirement expenses of $103,376 which is 90% of your last year's income of $114,862.

Retirement savings runs out at age 74.

Not including Social Security benefits.

Sally vs Bob.

Sally saved $2,227,052 and Bob saved $742,351 for retirement, a difference of $1,484,701. Sally saved $625 a month and Bob saved $208 a month (in the first year), a difference of $417 a month. That is the difference between a $150,000 mortgage and a $250,000 mortgage.

Sally and Bob live in the same city. Earn the same income. But Bob likes to spend money, with credit, student debt, a more expensive home, new cars and leases, vacations, out to eat several times a week, subscriptions to make his life a little bit more convenient and he impulse buys at least once a week for fun.

Sally is a saver, she bought a modest home, used cars, she goes out to eat once or twice a month, no subscriptions because she is a “do it herself” kind of person, no student debt because she worked her way through college, and she only buys things that are useful.

The takeaway, Bob's retirement will only last until least 74 years old. Sally's retirement will last until she is 92 years old. And if Bob still has debt in retirement, his retirement will last even shorter. Sally does not have debt.

Bob will have to make sacrifices in retirement, Sally will not.

Building wealth and becoming a millionaire (or PPP equivalent) takes decades. It takes discipline and consistency. It takes frugality and an aversion to debt. Save as much as you can, invest it, have an emergency fund and stay away from debt (home is the exception)...these are the fastest ways to wealth... and a comfortable retirement.

Stay frosty people.

50% allocated to ph-fund

Hi @fijimermaid

It's hard for anyone not to understand if you explain it to them with numbers, and even so, there will be those who can't resist the temptation to throw all their money away at the slightest impulse. Most don't know how to handle debt, they are fearful to invest in anything. They do not find it hard to spend a large amount on a phone, for example, but in some course that teaches them to invest, even if they pay half of what a phone costs, it seems expensive to them, at least that is what I can see. This is a problem.

”Most don't know how to handle debt, they are fearful to invest in anything.”

I love the statement.

People give more value to money they've earned as opposed to credit they have not. So they hold cash, but spend credit.

And humans are very corporeal in how they view value. That is why we buy physical things. Something that we can touch and hold. House, car, food, etc… That is why crypto is a tough sell for some people, it isn't physical (even though most fiat transactions are not either).

And people tying up their cash in investments that they shouldn’t access for decades is tough also. For one, they can't physically touch Investments, and two, they can't immediately access that money to buy physical things.

@fijimermaid, You have given me something to think about... It is true, the human being is still very corporeal, he needs to touch, to see, to be able to somehow make it tangible.

Although less and less, it is also a reality, we have gradually adapted to the digital, but there is still a large part of the world's population that does not. But on the economic level it is another thing, people need to feel that they have control, access to their money, they also value it too much, I think that is a determinant in the fact that people can dare to let go of money to let it flow and reproduce.

It is a good topic... Thank you, I had never thought about it or seen it that way.

The points you raised are very important. Obviously, for someone to be financially free, he must learn to spend less than what he earns. And of course, other investments should be a must, not just having one stream of income.

Excellent read buddy. Thanks for sharing

Thank you very much @samminator.

@tipu curate

Upvoted 👌 (Mana: 2/5) Get profit votes with @tipU :)

Thank you @tipu.

Thank you @alokkumar121.

I think I kind of fear retirement. Not because of the age factor but more of what to feed the mind when there is nothing to do. I think I'd continue to work even after reaching the financial goals. But the work would just meant to keep me engaged and busy and not starve myself for the sake of money. That level of financial independence we all need to achieve sooner than later.

#affable #india

I agree. I think that I'll work just to keep my mind busy after I retire. So maybe, I will never “retire” :)

Yeah, I think of financial Independence (money) as giving me options. If I can't work anymore because of my health, or I want to sit on a beach somewhere, or play video games 24 hours a day and 7 days a week, haha, I want to be able to have that option.

Highly strong and realistic points you have pointed out for us, it is easier to spend money as it comes but it takes a considerable amount of intelligence to realize the need to save more.

It is easy to fall from a point of abundance to the point of going into debt immediately when there is no proper plan in place, but with a concrete plan even when things are not going so smooth, it is still very possible to navigate situations and bounce back on your feet.

Yeah, personal finance is mostly about behavior...a little bit about math. When people go into debt (which Is virtually everyone at some point in their lives, including me), it is about impatience, greed and a certain degree of arrogance.

Spending less than I make and having a budget involves humility. Humility in the sense that I don't know what the future will be, so I better have some money just in case :)

And thank you @gbenga.