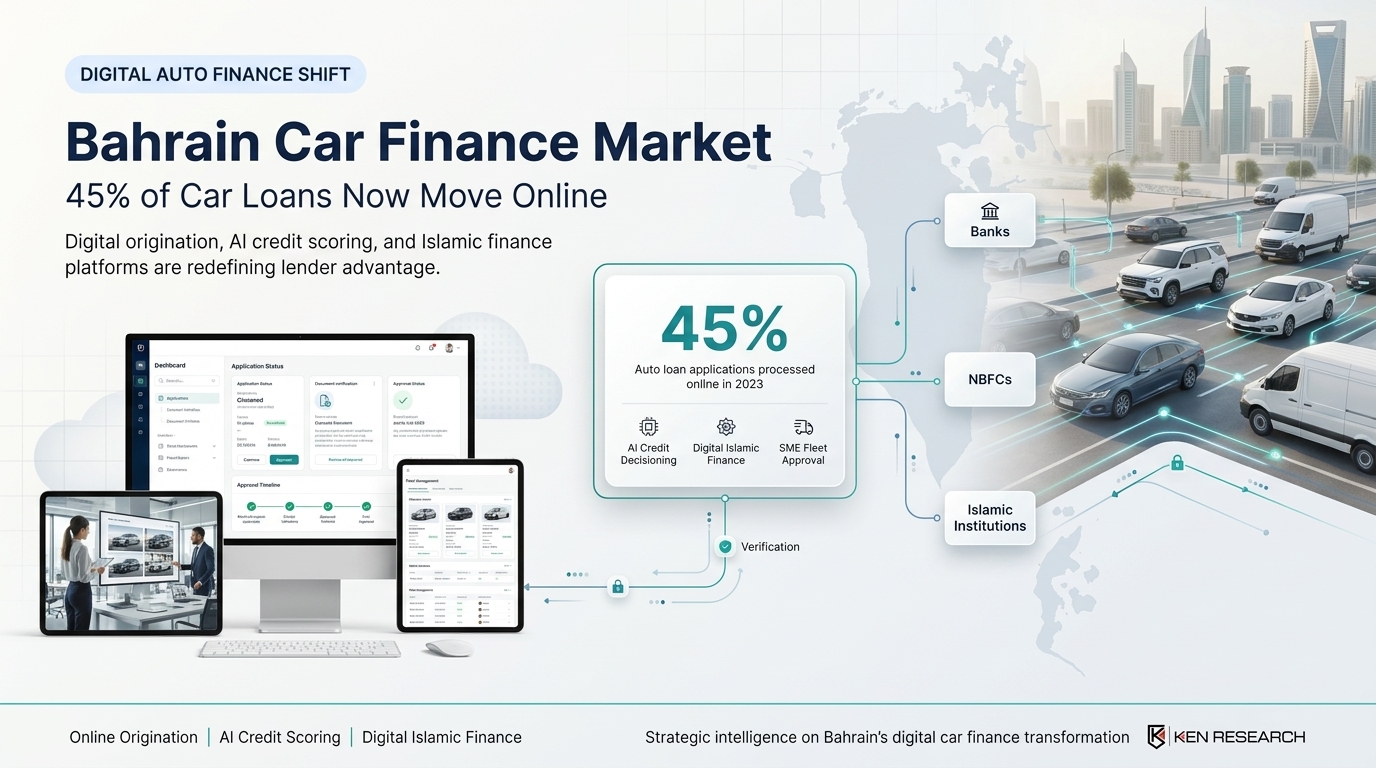

Bahrain Processes 45% of Car Loans Online - Ken Research on the Digital Finance Shift

In 2020, 25% of Bahrain's auto loan applications were processed digitally. By 2023, that figure had reached 45% an 80% jump in three years that is not a convenience upgrade but a fundamental restructuring of how lenders acquire, assess, and approve car finance borrowers. The implication for B2B buyers is direct: a corporate fleet manager who previously required in-branch visits, manual documentation submissions, and multi-week approval cycles can now initiate, complete, and receive approval for a multi-vehicle financing facility from a desktop interface. The implication for lenders is equally direct the institutions that built digital origination infrastructure early are compounding a distribution advantage that branch-centric competitors cannot rapidly close.

These competitive dynamics, digital platform adoption data, and the strategic implications for lenders and B2B buyers are mapped in the Bahrain Car Finance Market analysis by Ken Research. The report covers how banks, Islamic financial institutions, and NBFCs are deploying digital lending platforms to compete for new and used vehicle financing across individual, SME, and corporate segments. Ken Research provides the full competitive intelligence this blog draws from.

What the 45% Online Origination Rate Means for Lender Strategy in Bahrain

The shift to digital origination is not uniform across Bahrain's car finance lenders and the gap between early movers and laggards in digital infrastructure is widening the competitive distance between them in ways that are increasingly difficult to reverse.

AI-Powered Credit Decisioning and Approval Speed as a Competitive Weapon

The core competitive advantage of digital-first car finance platforms is approval speed. Bahrain's leading digital lenders are deploying AI-powered credit scoring models that process employment verification, banking transaction history, vehicle valuation, and CBB credit bureau data simultaneously reducing loan approval timelines from days to hours. For a B2B fleet operator requiring financing approval for 5 vehicles before a logistics contract commencement date, the difference between a 24-hour digital approval and a 7-day branch-based assessment is operationally critical. As Ken Research highlights in its competitive analysis, the Bahrain car finance market is experiencing a structural shift toward digital origination that is forcing conventional lenders to accelerate platform investment or cede the fastest-growing borrower acquisition channel to more agile competitors.

Transparency Regulations as a Digital Adoption Catalyst

The Central Bank of Bahrain's Consumer Protection Directorate regulations which require all auto finance providers to offer clear disclosure on loan terms, interest rates, and total financing cost have created a regulatory tailwind for digital platforms. When every lender is legally required to disclose the full cost of borrowing, digital comparison interfaces become the most efficient tool for borrowers to identify the lowest-cost option. The result is an accelerating flow of loan applications through digital channels, where comparison is frictionless, rather than through dealership finance desks where pricing opacity historically served lender interests. With 85% of lenders reporting full compliance with CBB consumer protection regulations in 2023, the regulatory standardisation is making digital comparison credible and actionable for borrowers at scale. The broader digital finance infrastructure this is building upon is documented in the Bahrain Sustainable Finance Market analysis by Ken Research, valued at USD 1.7 billion, which covers the ESG and digital finance regulatory convergence shaping Bahrain's financial services architecture.

How B2B Fleet Buyers Are Using Digital Car Finance Platforms in Bahrain

The B2B use case for digital car finance is structurally different from the consumer use case and most platforms are still optimised for individual borrowers rather than for the multi-vehicle, multi-stakeholder approval workflows that corporate and SME fleet buyers require.

SME Fleet Financing and the Digital Approval Gap

Bahrain's SME sector operating under a 2023 regulation mandating banks to allocate a minimum of 20% of lending portfolios to SMEs is a significant and growing car finance customer segment. A logistics SME adding 4 commercial vehicles, a construction contractor financing 6 utility vehicles, or a healthcare services company replacing its patient transport fleet all require financing decisions at business timescales not the consumer lending timescales that most bank origination systems are calibrated to. Digital platforms that offer multi-vehicle application workflows, consolidated documentation portals, and same-day approval for pre-qualified SME borrowers are capturing this segment systematically. As documented in the Bahrain car finance competitive analysis by Ken Research, the digital channel is the primary mechanism through which NBFCs are building SME market share against established banks. The Bahrain SME Financing Market analysis by Ken Research, valued at BHD 1.2 billion, provides the SME credit demand context within which digital car finance is competing for enterprise borrowers.

Digital Islamic Car Finance The Intersection That Determines Market Leadership

The most strategically important digital car finance development in Bahrain is the migration of Islamic finance products online. With 35% of auto loans structured under Sharia-compliant principles, lenders that can originate, document, and approve Murabaha and Ijarah contracts through fully digital workflows are serving the market's two fastest-growing demand characteristics simultaneously digital preference and Islamic finance preference. Bahrain Islamic Bank (BisB) and Kuwait Finance House (KFH) are investing in digital Sharia-compliant origination platforms that eliminate the in-branch Sharia compliance documentation requirement that historically added friction to Islamic car finance applications. As Ken Research identifies, this digital-Islamic convergence is the defining competitive frontier in the Bahrain car finance market the institutions that master both will disproportionately capture the market's growth through 2030.

The Challenges That Are Moderating Digital Car Finance Growth in Bahrain

Digital transformation in Bahrain's car finance market is not frictionless. Three structural challenges are moderating the pace of digital adoption and creating execution risk for lenders investing in platform development.

- NPL Risk in Digital Origination: The non-performing loan rate reached 8% in 2023 a figure that is partly attributable to the lower friction of digital loan origination enabling borrowers with marginal credit profiles to apply and receive approval without the relationship friction that branch-based lending imposes. Lenders scaling digital origination without proportionate investment in AI-driven risk assessment are taking on credit quality risk that will manifest in NPL increases. The institutions managing this most effectively are deploying dynamic credit models that incorporate real-time transaction data from the Bahrain Credit Reference Bureau rather than static income verification snapshots.

- Used Car Financing Complexity Online: While digital origination works well for new car financing where dealer networks provide standardised vehicle documentation, used car financing presents additional complexity. Around 30% of auto finance consumers in 2023 faced difficulties securing used car loans due to stricter credit policies and the higher collateral valuation uncertainty of pre-owned vehicles. Digital platforms have not yet resolved the physical inspection and valuation requirement that anchors used car credit decisions making used car financing a partially digital process that still requires human intervention at the collateral assessment stage.

- Cybersecurity and Data Protection Compliance: The CBB's Cloud Computing Regulatory Framework and consumer data protection requirements impose compliance standards on digital car finance platforms that increase operational costs. Banks reported a 15% increase in compliance costs in 2023 with digital platform security and data governance accounting for a significant share of that increase. For smaller NBFCs investing in digital car finance origination, this compliance overhead is a structural cost disadvantage versus the larger institutions that can spread the investment across broader loan portfolios.

If you are evaluating digital lending strategy, platform investment decisions, or competitive positioning in the Bahrain car finance market, speak to a strategic consultant to develop a data-backed market strategy.

Conclusion

The 45% online origination rate in Bahrain's car finance market is both a milestone and a competitive inflection point. The lenders that built digital infrastructure when origination was 25% online have compounded a distribution advantage over 3 years that translates directly into lower acquisition costs, faster approval cycles, and higher application volumes. The next competitive frontier digital Islamic car finance is being contested now, and the institutions that master Sharia-compliant digital origination will capture a market where digital preference and Islamic finance preference are both structurally growing simultaneously.

The full digital platform analysis, lender competitive positioning, and segment forecasts for the Bahrain car finance market are documented in the analysis by Ken Research.

Frequently Asked Questions

How fast is digital car finance adoption growing in Bahrain?

According to Ken Research, 45% of auto loan applications in Bahrain were processed online in 2023 up from 25% in 2020, representing an 80% adoption increase in three years. This shift is driven by AI-powered credit decisioning enabling same-day approvals, CBB transparency regulations making digital rate comparison credible, and B2B fleet operators demanding financing workflows that match business operating timescales rather than traditional branch-based lending cycles. The Bahrain car finance market is experiencing digital origination as its primary competitive frontier, with the gap between early-mover and laggard lenders widening.

Which digital lenders are leading Bahrain's car finance market transformation?

Ken Research highlights that Bahrain Islamic Bank (BisB), Kuwait Finance House (KFH), and digital-forward NBFCs are leading the digital car finance transformation deploying AI credit scoring, online documentation portals, and digital Islamic finance origination workflows that reduce approval timelines from days to hours. National Bank of Bahrain (NBB) and Ahli United Bank (AUB) are investing in platform upgrades to defend branch-network market share against these more agile digital-first competitors targeting the SME and individual consumer segments simultaneously.

What challenges are moderating digital car finance growth in Bahrain?

As per the Bahrain Car Finance Market analysis by Ken Research, three challenges moderate digital growth: an NPL rate of 8% attributable partly to lower-friction digital origination enabling marginal borrowers, the unresolved physical collateral inspection requirement for used car financing that limits full digital origination, and a 15% increase in compliance costs imposed by CBB's consumer protection and data governance regulations creating a disproportionate compliance burden for smaller NBFCs investing in digital origination infrastructure.

How does digital car finance benefit B2B fleet operators in Bahrain?

Ken Research's B2B segment analysis reveals that digital car finance platforms benefit SME fleet operators and corporate buyers through multi-vehicle application workflows, consolidated documentation portals, and same-day approval capabilities that align with business operating timescales. The 2023 CBB regulation mandating banks allocate 20% of lending to SMEs has increased credit availability and digital platforms are the primary channel through which SMEs are discovering and accessing these expanded financing options, particularly in the Bahrain car finance market's growing used commercial vehicle segment.