April global supply and inflation review for Proposal #117: 1.5 million SBD reduction, little change in STEEM growth rate

Overview

Proposal #117 runs from December 26 through June 26, burning 10K SBDs per day from the Steem Proposal System as either STEEM or SBD. The proportion of STEEM and SBD to be burned is controlled by a multikey wallet that's operated by Steem top-20 witnesses. When the proposal began, 25% of SBDs were burned as STEEM. After a short time period, the ratio was raised to 50/50, and that's where it has remained. So, each day the proposal burns 4992 SBDs and 4992 SBDs worth of STEEM.

After almost four months of the six month proposal, it's time for another look at where things stand.

At this point, my main observations are these:

- Despite burning somewhere around 40K steem per day for four months, the overall STEEM supply does not seem to be affected by the proposal.

- The SBD supply has shrunk by about 1.5 million.

- Functionally, it turns out that proposal #117 and proposal #116 have been, basically, equivalent (except that the daily amounts and durations were different). The fundamental net effect is redistribution of value from burned SBDs to the ones that remain.

I believe that the reason for this is that in order to burn STEEM for proposal #117, SBDs from the SPS need to be sold for STEEM. After selling their STEEM, the traders on the other side of those transactions need to replenish their STEEM holdings. Instead of buying STEEM on the internal or external markets, the traders have been converting SBDs into STEEM. These conversions basically transform the proposal's STEEM burns into SBD burns.

The follow-on effects, then, appear to be these:

- Inflation has remained close to the blockchain's expected rate.

- The haircut price has fallen by almost 15% from about $0.136 to about $0.116.

- The blockchain conversion rate of SBDs in terms of STEEM has increased by ~16% from 7.35 to 8.56 STEEM per SBD.

| Metric | Before Prop #117 | Current (April 2026) | Change |

|---|---|---|---|

| Haircut Price | ~$0.136 | ~$0.116 | -14.7% |

| STEEM per SBD (conversion rate) | 7.35 | 8.57 | +16.6% |

| SBD Supply | (Baseline) | -1.5M | Significant Drop |

| STEEM Supply | (Baseline) | +13.7M (~300k above expected inflation) | Close to expected |

| SPS SBDs | 4.2M | 3.1M | -26% |

| SPS Market Value | $2.0M | $1.6M | -20% |

So, let's move on and look at some charts.

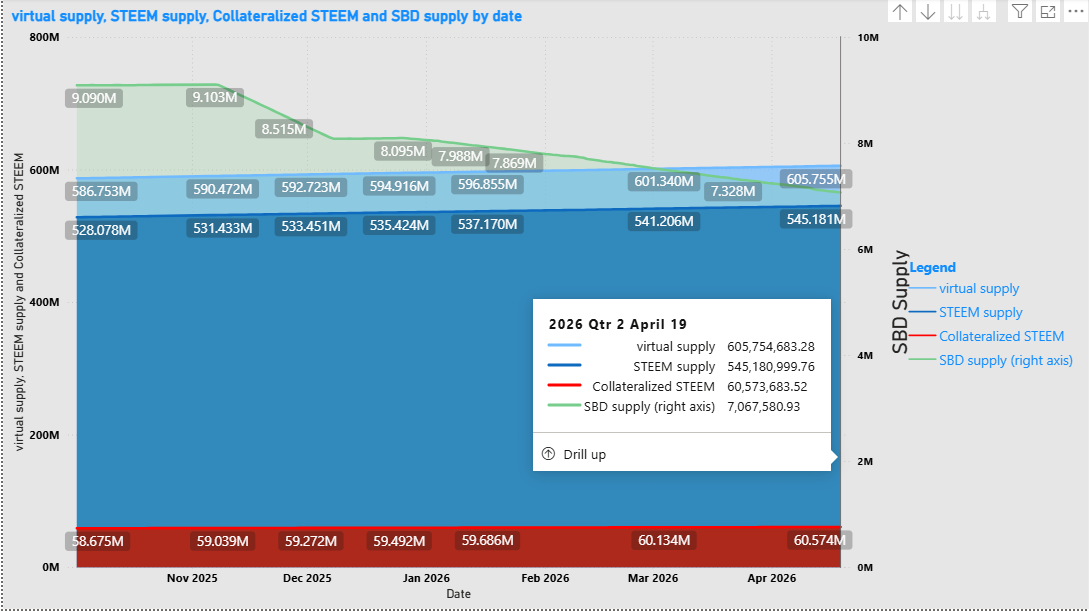

Global Properties

As expected, the change in SBD supply is visible (the SBD supply axis is on the right), but the change in the STEEM supply is not (axis on left). This is simply because the SBD supply is a much smaller number. The graph shows steady SBD supply growth heading into proposal #116, then a drop while that proposal was running, followed by more growth into proposal #117. After proposal #117 began, the supply has been falling steadily again.

The combined effect of proposal 116 and proposal 117 has reduced the overall SBD supply by about 2 million.

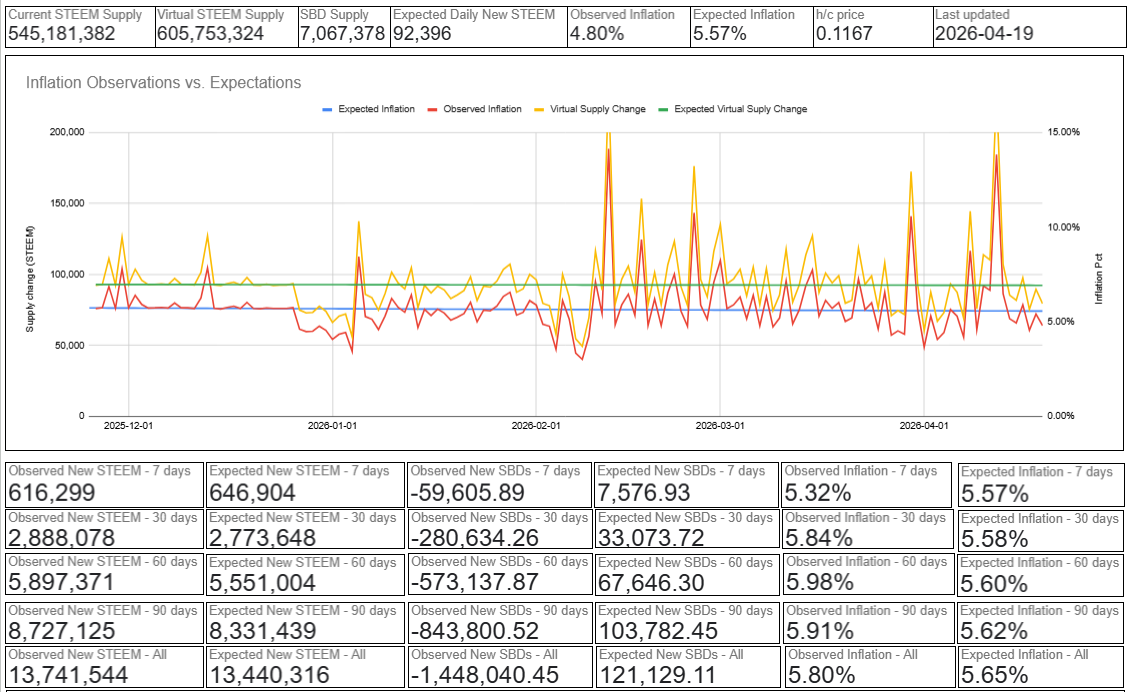

Observed inflation vs. expected inflation

Here we see that despite some peaks and valleys, inflation at longer time scales has been fairly close to the expected rates. With STEEM supply growth of about 300K above expectations, the overall supply increased by only about 2% more than expected (reminder: SBD conversions increase the inflation rate). On the other hand, the SBD supply is about 1.5 million lower than the expected value. Instead of growing by 121K, it declined by more than 1.4 million.

The visuals in this section are updated daily, and they can be found here

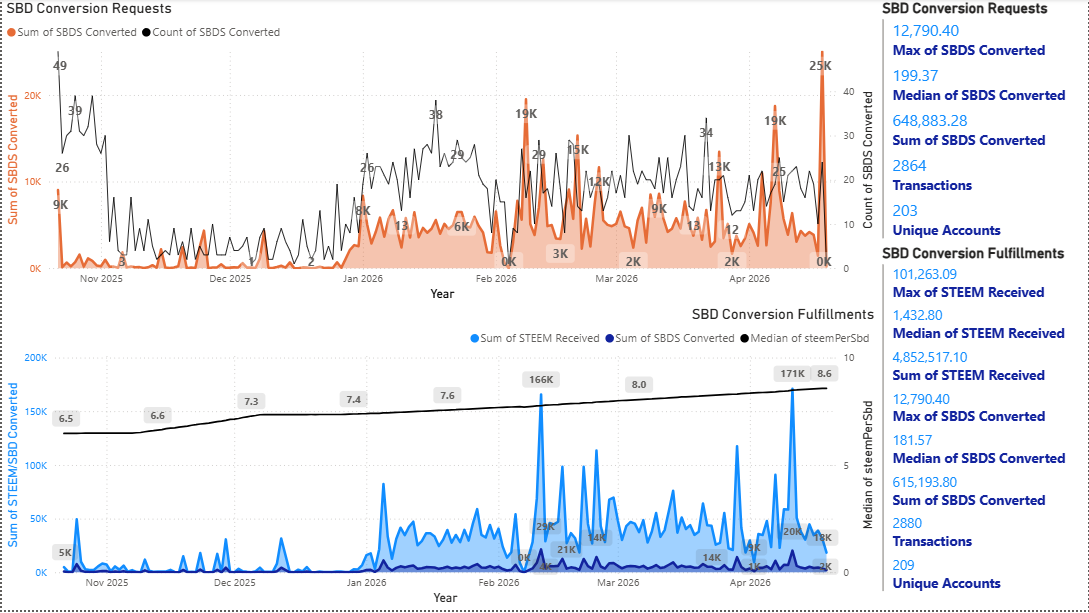

SBD Conversion Activity

180 days

While not definitively proven, the timing at this scale strongly suggests that proposal #117 coincides with a behavioral shift among some trading accounts. SBD conversion had tapered off during the second half of 2025, but it ramped up again starting in January, and it has remained elevated since then. A couple weeks ago, I thought that it might be tapering off again, but that seems not to be the case.

A new peak was registered on April 18, so we can expect inflation to be elevated on Monday or Tuesday this week.

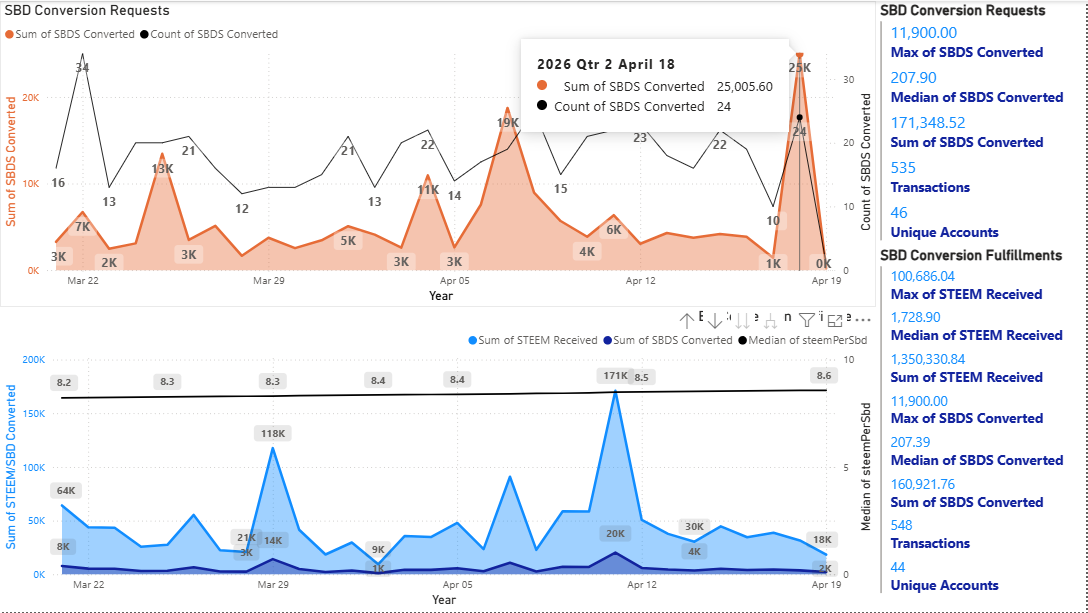

30 days

The 30 day time scale reinforces the notion that the trend in SBD conversions may be flat or growing.

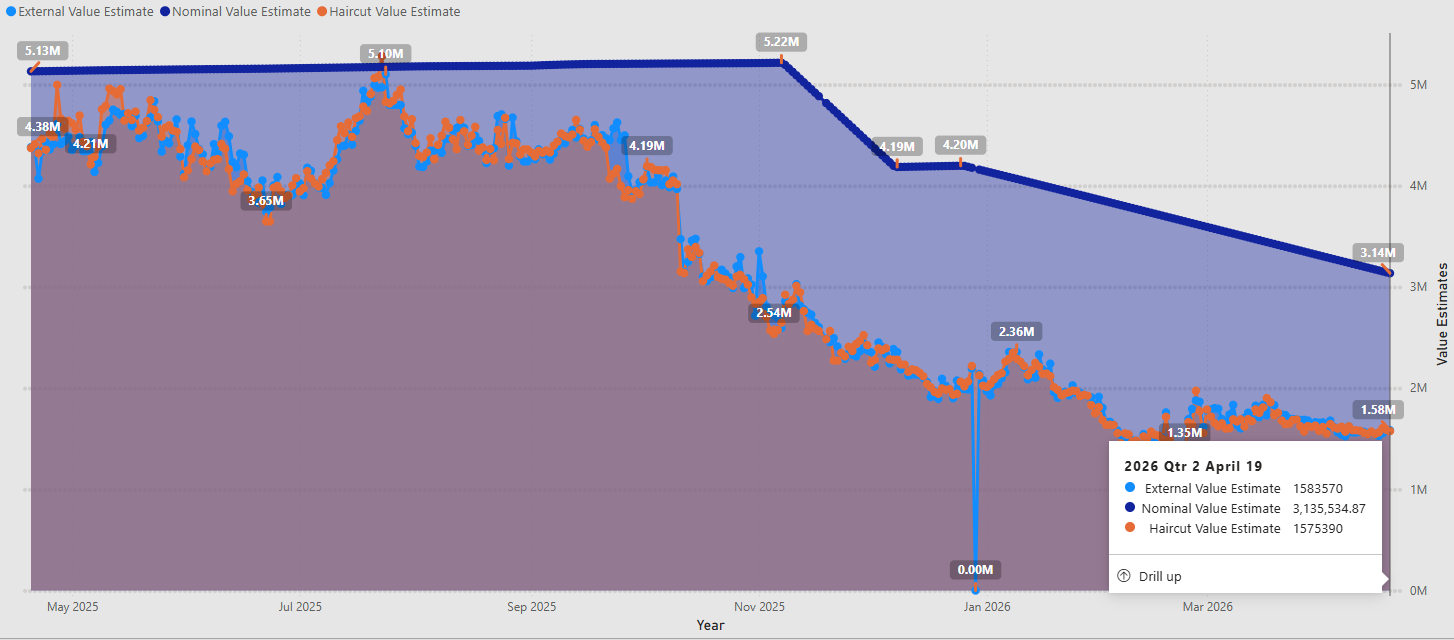

Internal, external, and nominal value of the SPS Wallet

As the STEEM per SBD ratio increases, value is redistributed from the burned tokens to the remaining ones. Thus, the gap between the nominal value and the market value is continuing to shrink.

My theory continues to be that the SBD market price is following a sliding peg that's given by the ratio of the (average) STEEM price divided by the haircut price. At today's values, the STEEM price is $0.059 and the haircut price is $0.116. This would predict an SBD market price of $0.509. The actual SBD market price is $0.505. (note I don't necessarily expect that behavior to continue if the STEEM price rises above the haircut price for any sustained time span.)

The internal and external market values of the SPS have been tracking closely and moving in parallel ever since last year's upbit delisting of the SBD.

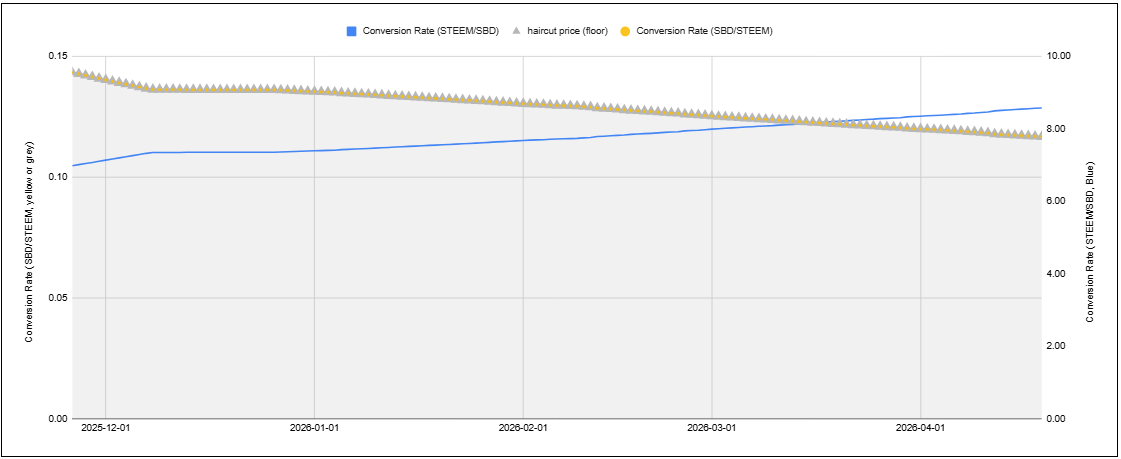

Haircut pricing / SBD Value

This shows the declining haircut price over the course of the proposal (and before, including the tail end of proposal #116). It also shows the corresponding increase in the conversion rate of STEEM per SBD. At the start of proposal, converting one SBD into STEEM would have yielded about 7.35 STEEM. Today it would yield about 8.57.

We see sharp slopes at the end of proposal #116, a leveling off between proposals, and then gentler slopes during proposal #117.

The conversion rate in terms of SBD per STEEM (yellow) is currently tracking with the haircut price (grey). If/when the STEEM price rises above the haircut price, I believe that those two values will diverge, and the conversion rate will rise above the haircut value. Similarly, if the STEEM price rises above the haircut price, I believe that the STEEM per SBD value would start tracking the actual STEEM price, instead of the haircut price.

The visual in this section is updated daily, and it can be found here

Conclusion

One goal at the start of the proposal was to reduce inflation by burning SPS funds as STEEM, instead of SBDs. As a first order effect, it does this. However, due to SBD second order conversion activity the inflation reduction is offset by SBD conversions. Instead, on net, what proposal #117 seems to accomplish is to lower the haircut price and reduce the SBD supply at a somewhat faster rate than if the SBDs had been burned directly. This may be done by a stimulatory effect on SBD conversion activity.

It remains to be seen if the elevated conversion activity will be sustained after the end of the proposal.